Employee Benefits

AG EB ONLINE

Published on 21/01/2021

SHARE

Supplementary pension: facts and figures

How many group insurance plan members are there in Belgium? What’s the total combined value of supplementary pension savings, and are there any differences by age and gender? These questions are addressed in new research by the Financial Services and Markets Authority (FSMA), based on Sigedis data. In this article, we look at the key figures from the study and the factors behind them.

How many group insurance plan members are there in Belgium? What’s the total combined value of supplementary pension savings, and are there any differences by age and gender? These questions are addressed in new research by the Financial Services and Markets Authority (FSMA), based on Sigedis data. In this article, we look at the key figures from the study and the factors behind them.

Supplementary pension: facts and figures

3,950,000 Belgians were members of a pension plan in 2020 – a 5% increase on 2019. The total combined value of pension savings was €91.5 billion – 7% higher than the equivalent figure for 2019.

How do the figures stack up at AG?

Half of large Belgian corporations use AG as their employee pension plan provider. This means that 1,195,000 people are members of an employer-sponsored and/or sector-wide retirement and death-in-service plan provided by AG.

The supplementary pension: what factors underpin these findings?

1. Age, gender and employment status

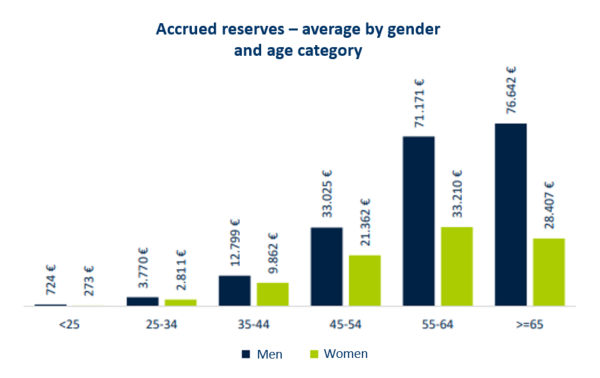

The older the plan member, the more accrued reserves they have. People build up their reserves steadily throughout their career, forming a nest egg to fund their retirement. On average, members aged 55-64 years have accrued reserves of €56,057. Men in this age group have accrued twice as much as women (€71,171 vs. €33,210).

Source: “The second-pillar pension in images - Sectoral overview 2020” (available in French and Dutch only).

What does AG offer?

With AG, you can follow an investment strategy that evolves in step with your staff member’s age.

The study also reveals that the share of supplementary pension plan members differs by employment status. The overwhelming majority are wage earners, who save for retirement through group insurance plans. Conversely, only 9% of supplementary pension plan members are self-employed – and those with mixed careers (combining wage earning and self-employment) make up an even smaller share.

- 85% of members are wage earners

- 9% of members are self-employed

- 6% of members are people with mixed careers

Of the €91.5 billion in combined accrued reserves in Belgium, 69% were paid in by wage earners and 31% by the self-employed.

2. Plan sponsor

Plans can be sponsored either by an employer or by a sector. Employer-sponsored pension plans are known as corporate plans. Pension plans sponsored by an entire sector, meanwhile, are known as sector-wide plans.

Overall, there are more members of sector-wide plans, although their accrued reserves are lower than for members of corporate plans.

| |

Corporate plans |

Sector-wide plans |

|

Number of members |

1,991,464 |

2,113,657 |

|

Accrued reserves – combined total |

€52.8 billion |

€5.2 billion |

|

Accrued reserves – average per member |

€27,237 |

€2,475 |

|

Accrued reserves – average per member aged 55-64 years |

€69,179 |

€4,715 |

What about AG?

At AG, we help employers and entire sectors set up pensions, and we have a solid track record in managing both corporate and sector-wide plans. For you, this means professional support and expertise tailored to your exact requirements.

3. Types of pension plan

There are two types of pension plan:

• Defined-contribution (DC) plans:

Under a defined-contribution plan, the employer or sector commits to contributing a certain amount, but makes no promise as to the final value of the pension.

• Defined-benefit (DB) plans:

Under a defined-benefit plan, the employer or sector promises that the member will receive a particular lump sum or regular annuity when they retire.

More people pay into a defined-contribution plan than a defined-benefit plan. Yet accrued reserves for DC plan members are substantially lower than for DB plan members.

| |

DB plans |

DC plans |

| Share of members |

5% |

77% |

| Accrued reserves – combined total | €20.0 billion | €33.6 billion |

Our solutions

With AG’s DC plan solutions, you can choose to invest in Branch 21 funds, Branch 23 funds or a combination of the two.

We also offer a third option, Cash Balance, which lets you choose the financing fund you want to pay into, and decide what return you want for your staff members. And if your accrued reserves exceed your commitments towards your staff, you decide how the surplus is used.

4. Investing in Branch 21 funds, Branch 23 funds or a combination of the two

Insurers manage 82% of accrued reserves (€74.6 billion), with pension funds managing the remaining 18%. Insurers invest the vast majority of these reserves (€67.3 billion) in Branch 21 funds, and €6.7 billion in a combination of Branch 21 and Branch 23 funds. The remainder (€0.6 billion) is invested in Branch 23 funds.

Source: “The second-pillar pension in images - Sectoral overview 2020” (available in French and Dutch only).”

Which option should you choose with AG?

With AG, you can opt to invest in Branch 21 funds, Branch 23 funds or a combination of the two.

A Cafeteria Plan offers even more choice: staff members can make their own investment decisions within the parameters you set.

Want to find out more about the FSMA study? Read the full 2020 survey here (available in French and Dutch only).